YTD

The following is a letter from an institutional investor who prefers to remain anonymous. He probably doesn’t want to be tracked by private investigators..

Despite concluding the one-day trial, the fate of Proposition Four is not likely to be determined for a long time. As the judge mentioned, whichever party loses in his court will likely appeal the decision to the Delaware Supreme Court. Win or lose, there is one outcome from the trial and the events that preceded it that is certain, the reputations of management and the board of directors were severely damaged.

Let us recap the events and discoveries that led to the damaged reputations:

-To start with, by proceeding with the lawsuit, the board has ignored the wishes of shareholders who voted against Proposition 4 – the vote results were ~65% against.

-The board approved the use of, at least deceptive, and at worst untrue, statements in proxy statements.

-The board subpoenaed several shareholders of the company, which presumably caused those shareholders to incur legal costs in order to comply with the subpoenas.

-The board approved the hiring of a private investigator to investigate at least one of the company’s shareholders.

-It became abundantly clear that the intent of Proposition 4 was not to implement a stock split, but to provide acquisition currency to the company. It is not a stretch to say that the marketing of this proposition to investors was deceptive.

-The board’s capital allocation decisions were tarnished as it was revealed that one of the acquisition targets was a collection of assets from Occidental Petroleum – Occidental knows their drill plans better than anyone, which means the buyer of royalty assets from them are not likely getting the better end of the deal.

-The board and management look to be poor stewards of financial resources given the use of a private jet as a means of transportation to Delaware and hiring an army of attorneys and paralegals to show up in court.

-The deposition of the co-chairman came across as arrogant and indifferent as to the wishes of the shareholders.Controversy has surrounded this board since its inception, as shareholders do not feel adequately represented. This point is clear from the last shareholder meeting in Dallas and should be clear from the shareholder representation in the courtroom this week. I do not know if the two co-chairs can rehabilitate their reputations with shareholders. That will be determined in the next election for directors. It may not be too late for the other directors to rehabilitate their reputations. Here are some suggestions for how to do it.

To start with I would:

-Not support an appeal if the defendants prevail.

-Ratify the de-classification vote. This was voted on by shareholders and passed. I could see delaying this until the meeting was fully concluded, but as the judge said, having another meeting date is moot at this point. Given this, ratify the de- classification of the board.

-Pay for the legal expenses of the shareholders you subpoenaed.

-Issue an apology for the shareholder you investigated.Longer term I would:

-Cease searching for large acquisitions. Shareholders do not want the company executing large acquisitions.

-Given the above, it is likely that you can cut expenses associated with finding large transactions.

-Align management’s compensation with activities that they can control and not with metrics tied to the changing price of oil or completing acquisitions.Being respectful and having a less arrogant tone when dealing with shareholders would also go a long way. I hope that you, as board members, take the above into account and repair your reputation with shareholders, which could lead to long board tenures for you. Contentious situations often cause parties to dig their heels in. I would encourage you to look at the vote of the shareholders, remember the comments from the annual meeting, appreciate how many shareholders took the time to attend the trial, and rise above any temptation to dig your heels in.

Again, taken from the comment section of a prior post.

The text below was copied from the comment section of a prior post. Thank you to the author and thank you to all of the shareholders who packed the court room Delaware today.

I was present in the courtroom today. A few things I learned…

First, do not expect a ruling any time soon. The parties will decide how to do post-trial briefs for the judge tomorrow. That will impact if those briefs are done before the next scheduled meeting.

The judge seemed to indicate that the future meeting would be a moot point. If he rules for TPL, then Prop 4 will effectively be deemed passed. If he rules for HK/SV, then Prop 4 is effectively dead.

The judge also seemed to think the date of record currently set for voting on the proposal was too far in the past. However, the point is likely moot based on either ruling.

My hunch is that the judge is inclined to rule for HK/SV. However, he will be mindful of any precedent that a ruling could set for broader Delaware Corporate law. I suspect he will look for a narrow issue that allows him to rule for HK/SV that does not have broader implications.

***

A few things I’ve learned: TPL has spent north of $6, probably closer to $10 million of shareholder money on litigation.

TPL – through its law firm, Sidley Austin – hired a private investigator to determine if Lion Long Term Partners colluded with HK/SV in releasing its pre-vote statement.

The courtroom was over capacity. A reporter for Bloomberg Law said she has never seen so many shareholders appear in person. No shareholders present indicated support for TPL management.

This was probably the first time in years people were sitting on the floor in the Delaware Chancery Court. The floor and benches do not appear to offer different levels of comfort.

The judge referenced the crime-fraud exception to pierce attorney-client privilege TPL asserted on one its documents.

The statement in question was in a proxy statement: “The Company currently does not currently have sufficient shares available for issuance to meet its existing obligations. We are concerned that the Company is unable to meet its current and potential obligations and believe it is important that the Company obtain additional common shares available for issuance in the future.”

Director Karl Kurz testified that the quote in the proxy did not appear to be accurate. TPL’s lawyers tried to rehabilitate this later.

EO and MS were excellent witnesses. (Humorosly they were quite a contrast. New York HK and West Texas EO.)

The TPL lawyers, at times, came across like high school mock trial participants. They seemed to be trying to create drama and theatrics where none existed.

TPL management does not appear to be a fan of the TPLT Blog. (Ty, Michael, John & David – nice to meet you via blog. I wish it hadn’t come to this.)

My hunch has been that management wants to do an acquisition to dilute HK/SV. Nothing I saw today has changed my opinion.

The trial also convinced me that no one knows TPL better than EO. He and MS are genius-level folks. It had to be unnerving for opposing counsel to be in a situation where the witness was clearly more intelligent than the lawyer asking the question. That’s not something you see all the time.

By my count there were around 25 attorneys and paralegals there on behalf of TPL. And, as shareholders, we are collectively paying for them to sue the majority of voters.

The expert witness testimony led me to believe this is not a slam-dunk case. Clearly I think HK/SV should win. However, the judge will be thinking about more than just this case. There’s a reason companies choose Delaware. This is why I suspect he will find a narrow point that favors HK/SV and use that rather than staking out new law.

***

As TPL shareholders we all owe MS & EO a debt of gratitude for spending the huge amounts of money to fight this fight. While they have their own reasons, everyday retail investors are free-riders on their dime.

“Maverick, it’s not your flying, it’s your attitude. The enemy’s dangerous, but right now you’re worse. Dangerous and foolish. You may not like who’s flying with you, but whose side are you on?” – Iceman on foolish spending of shareholders funds and poor corporate governance

I’m reading them at the same time as you. Don’t be shy about sharing findings in the comments!

“After all, for Proposal Four to succeed, an absolute majority of TPL’s outstanding shares were required to be voted in favor of the proposal.224 In fact, only about 35.18% of TPL’s outstanding shares were voted in favor of the proposal.” pp60, Defendant’s Brief

Afternoon Haiku:

TPL ordered

Disclosure is important

The shareholders smile

Fun read here. Enjoy!

I’ve been told the answer to ballot questions is “call Mackenzie”. The company telling you contact the proxy solicitor is par for the course. A company with real care for its investors would want to eliminate any lack of clarity. So typical.

I would not be surprised if they instructed the solicitor to send the whole ballot out again even though #4 is the only vote still alive. If I were them, I would do this to draw attention away from #4 to make it look routine when it is anything but. If I were them, I would be hoping to catch some unengaged voters sleeping.

The first time I voted, this is what I cast. https://tpltblog.com/2022/10/17/my-ballot/

Fill in all the dots. Enjoy voting against most of the incumbents and the executive comp question again. It’s meaningless but fun.

#4 is where your vote matters. Contact your broker to make sure that vote gets counted.

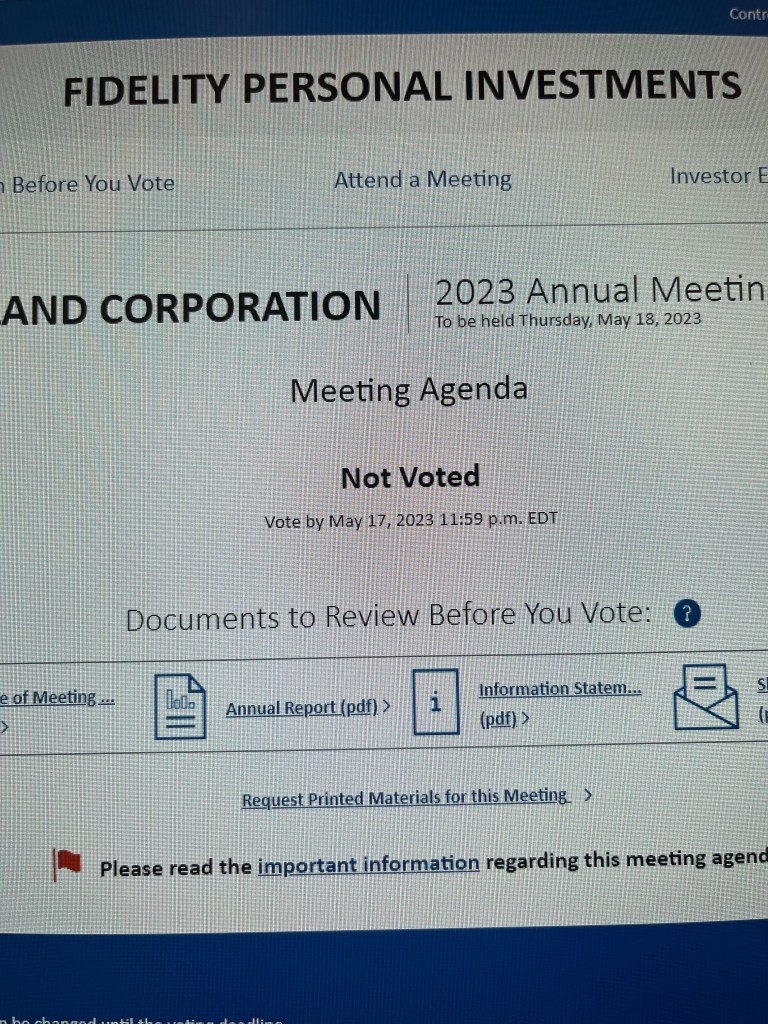

These Merrill and Fidelity emails link me to a voting portal where it clearly says “Not Voted” on the ballot.

This is the exact same ballot as last fall.

What’s going on? I already voted this ballot.

If you contact IR to get to the bottom of this, please let us know what they say.

From reader James:

The guys at Special Situation Investing have been following TPL closely and giving good insights.

There are two more links in the comments of the previous post but I’m writing this from my phone and I’m cut/paste challenged right now.

Below is a letter from a reader. I’m posting to see if anyone else uncovered any issues in voting for the upcoming “meeting”.

Everything was smooth my end. Accounts at two different brokerages presented my prior votes to me. I made no changes.

Hi from Canada.

Two days ago I received voting instructions via snail mail, for May election, for 4 of the 5 accounts in which I own TPL. I voted by phone these 4 accounts. In every case I was informed my shares had already been voted, but I was allowed to change them.

The fifth account where most of my shares are held did not get voting instructions via snail mail. However approximately 1 month ago I received via e-mail voting instructions for TPL. Today I attempted to vote these shares, turns out this was my fifth and largest account. The site was not live, however it said these shares had already been voted, and I was not allowed to change the vote whatever it was. I have contacted the company for assistance.

Seems all my shares were voted by someone other than me. Thought I’d put this out there to see if anybody else has had the same experience. Thanks.

Reader

Has anyone written to the board to request an investigation of the Manti Tarka dealings referenced by the defendants in their recent answer to complaint?

If you have, can you let me know if you’ve received a response? If you haven’t, it could be worth your time to do so.

You’d think a board with a fiduciary duty would want to investigate any whiff of conflicts of interest.

https://tpltblog.com/2023/01/11/defendants-answer-to-verified-complaint/