More transparency. Progress.

‘Tis a shame we have to be a month into a proxy battle to get information like this.

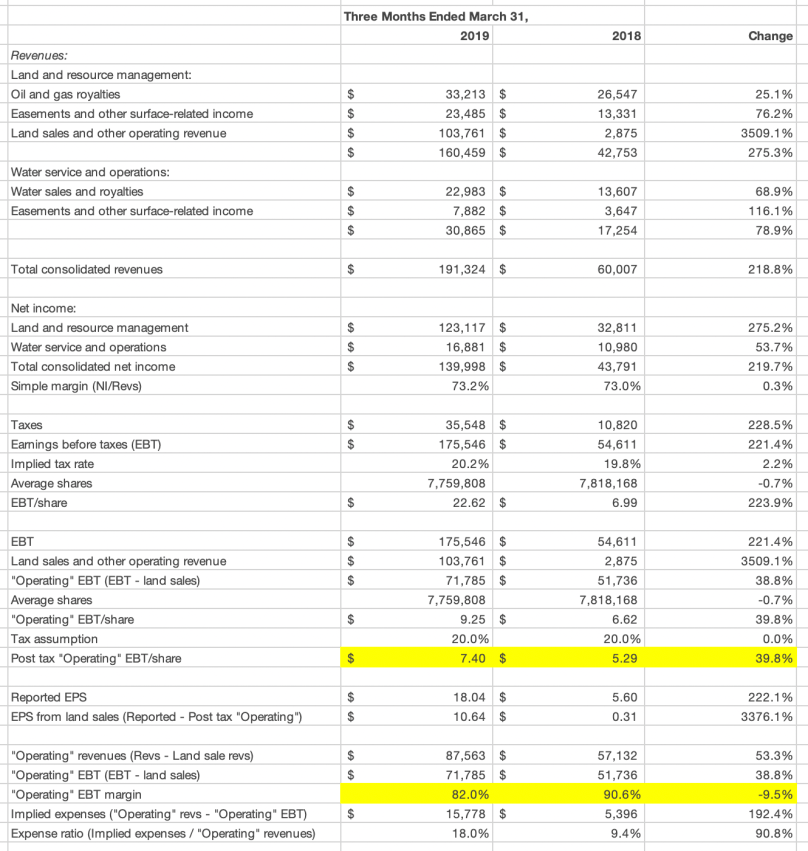

Notably absent are responses to the Preston Young/Sidra, Manti Tarka, and Peterson/Water questions.

Business Wire

DALLAS — April 23, 2019

Texas Pacific Land Trust (NYSE:TPL) (the “Trust”) today responded to several false or misleading statements recently made by dissident trustee nominee Eric Oliver regarding some of the Trust’s key transactions.

The Trust observed that Mr. Oliver either fundamentally misunderstands the business or intentionally misrepresents information about the Trust in an attempt to mislead investors – either of which should disqualify him from a seat on TPL’s Board of Trustees. The decisions made by TPL’s management, with the Trustees’ oversight, have clearly created and will continue to create long-term shareholder value. Mr. Oliver’s shockingly uninformed statements make it clearer than ever that shareholders’ best choice for their new trustee is General Don Cook.

The Trust further noted that Mr. Oliver’s lack of understanding of TPL’s business model should be concerning to shareholders. TPL pursues land sales opportunistically and only when there is a clear benefit to shareholders. Our strategy has been to consolidate acreage, invest in higher-return investments, or drive further development and revenues where TPL maintains royalty interests. It is this thoughtful strategy of deploying capital where it will create new value that has allowed TPL to deliver spectacular returns to shareholders.

2018 NPRI Sales Yielded Superior Acquired Acreage and Maintained Exposure to Portion of Sold Acreage

Mr. Oliver claims that the Trust sold non-participating royalty interests (NPRI) to Chevron in 2018 and lost the opportunity to capitalize on prime property. The truth is that the Trust performed a three-way swap with Chevron and Double Eagle Energy that enabled the Trust to use the sale proceeds to purchase a royalty position over 1.8x larger than the one it sold. Mr. Oliver also insinuated that much of the acquired acreage was located outside core areas of the Midland Basin; however, well results throughout a majority of the asset position have been very strong.

By completing this swap, the Trust was able to:

- Retain half of its NPRI under tracts of land that were part of the sale;

- Diversify holdings through exposure to a more varied set of blue-chip operators; and

- Achieve a net increase of 667 net royalty acres.

Much of the royalty acreage the Trust acquired in this swap was superior to the acreage sold, as the acquired acreage exhibits stronger recent well results and has significantly more producing wells and horizontal well permits. This is consistent with TPL’s core strategy of focusing on higher-return assets in strategically critical areas.

The Trust’s Surface Acreage Sale Yielded Tremendous Proceeds, Enabled Additional NPRI Revenues

Mr. Oliver also says that he would have voted against a sale of surface acreage to WPX Energy in January 2019. Once again, his position is dangerously uninformed. This transaction generated proceeds of approximately $100 million at an average price of $7,143 per acre in an area with high potential for drilling but with continued challenges from adjacent surface owners. The position sold was a non-contiguous “checkerboard,” and neighboring surface owners had historically obstructed development of the area. For these reasons, contrary to Mr. Oliver’s back-of-the-envelope calculation, the Trust was only receiving an estimated average of approximately $2.1 million in revenue over the last four years across the 14,000-acre position, which represents approximately $150 per acre.

Selling this acreage position allowed the Trust to monetize a non-core asset and re-deploy those proceeds into highly strategic surface acquisitions, which will enhance near-term opportunities for the water business. For example, the Trust has redeployed approximately $83 million of the $100 million of the sale proceeds in a tax-free 1031 Exchange, creating 53,000 contiguous acres in the core of the Delaware Basin1, including highly strategic acreage on the Texas-New Mexico border. This position is leased by blue chip E&P operators with large capital development budgets and best-in-class safety and environmental implementation.

In the long term, this transaction also protected the Trust’s competitive advantage by engaging with a counterparty that would not be adversarial to TPL’s interest in growing the water business.

In criticizing this transaction, Mr. Oliver apparently intended to represent his alleged expertise in oil and gas by describing pricing differentials for water in New Mexico and Texas, noting that prevailing water prices in New Mexico range from $2.00 to $2.50 per barrel. Mr. Oliver, however, has even these basic facts wrong.

Actual current water prices vary significantly in New Mexico. In eastern Eddy County, they are as low as approximately $0.50/barrel, rising to approximately $1.50/barrel in western Eddy County and northern Lea County. Although prices can reach the $2.00/barrel range under certain very specific circumstances (e.g., when an operator is bound to acquire water from a specific owner), these are not applicable to TPL.

Mr. Oliver falsely claims that the Trust’s sale of 14,000 acres created a “freeway” for other suppliers to transport water into New Mexico. That is simply not true. In fact, the Trust reserved strategic water rights in the sections adjacent to New Mexico. WPX acquired the land because it enhanced WPX’s ability to utilize its existing mineral rights below the adjacent landowner’s holdings, not for any reason related to the transportation of water.

Make Your Voice Heard

Mr. Oliver’s willingness to make misleading or entirely uninformed assertions like these should raise serious doubts about his knowledge of the Trust’s business, and his suitability for election as your next trustee.

The Trust urges shareholders to vote FOR four-star General Donald “Don” G. Cook using the BLUE proxy card. Shareholders can also read more information by visiting www.TrustTPL.com.

Shareholders can view a video Q&A with General Cook on Thursday, April 25 by visiting www.TrustTPL.com at 11:00 a.m. CT. A replay will be available beginning on Friday, April 26 on the website for those who are not able to tune in on Thursday. Shareholders who desire more information about General Cook’s background and his vision for TPL are encouraged to submit questions via email at AskGeneralCook@tpltrust.com by Wednesday, April 24 at 5:00 p.m. CT.

If you have any questions or need assistance in voting your shares, please contact the Trust’s proxy solicitor:

MacKenzie Partners

1407 Broadway, 27th Floor

New York, New York 10018

(212) 929-5500 or call Toll-Free (800) 322-2885

Email: proxy@mackenziepartners.com