https://www.bizjournals.com/dallas/news/2021/11/30/texas-pacific-land-corporate-governance.html

The company said in a prepared statement to Dallas Business Journal that its classified board structure was recommended while still a trust by the Conversion Exploration Committee. The committee was made up of trustees and investors, most of whom became board members. “The structure is intended to provide stability and continuity to ensure a smooth transition from a trust structure to a c-corporation, and to enable TPL Corporation to attract and retain highly qualified directors who have a focus on the long-term objectives of the company,” a Texas Pacific spokesperson said in a prepared statement to Business Journal.

Tim Schwartz, whose firm Schwartz Investment Counsel owns an almost-1% stake in Texas Pacific, said he was glad when the trust converted to a corporation. “I think that was a huge positive for the company,” Schwartz said. “But since then, I would say there’s been not as much progress as we would have hoped in terms of the corporate governance. And to us, it feels like the board is not that conducive to additional corporate governance improvements. The actions they’ve taken over the past few weeks, that just solidifies that opinion.”

James Spindler, the University of Texas at Austin Mark L. Hart, Jr. Endowed Chair in Corporate and Securities Law and a professor at the McCombs School of Business, said implementing a classified board like Texas Pacific’s can be controversial. Classified boards can entrench directors, protecting them from removal in hostile takeovers or proxy battles — like the one Texas Pacific faced two years ago.

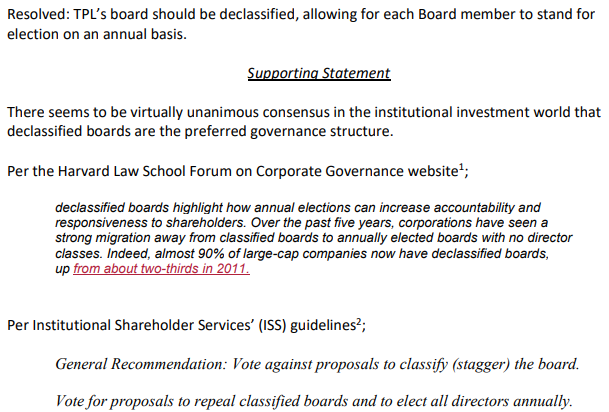

“There’s a general concern among reformers and activist investors, and I think in the larger corporate communities, that classified boards have some negative consequences,” Spindler said. “(They) tend to entrench management. So if you have management that’s making bad decisions, or making self-interested decisions, it’s a lot harder to kick them out.” Harvard Law School professors Alma Cohen and Director of the Program on Corporate Governance Lucian Bebchuk — experts on corporate governance — found through research that there’s a correlation between classified boards and “an economically meaningful reduction in firm value.”