We have some updates on outstanding shareholder proposals via the SEC No-Action Chart.

First, it appears as if the SEC has sided on behalf of TPL in concurring that there is basis to exclude the proposals of Special Opportunities Fund, Inc and Robert Zaccheo, Jr.

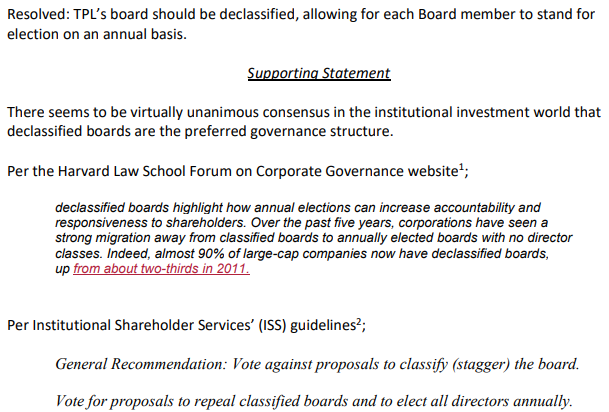

BUT, there is some light for the Declassify-the-Board proposal of Gabriel Gliksberg. The SEC chart indicates there is a revision that could be undertaken that would, in their eyes, make the proposal ineligible for exclusion.

ATG/Gliksberg took to Twitter to elaborate by posting the full reply from the SEC. The letter, dated 11/23, states that Gliksberg can cure the one basis for exclusion found by the SEC by modifying some language in the proposal that would allow for elected directors to not have their terms shortened should the proposal be successful. Gliksberg has a week to act.

I don’t remember electing any directors, but that’s beside the point.

Let’s say Gliksberg modifies the language. That gets us to 11/30. From there, the proposal gets into the new updated proxy which then goes right to the printer. Maybe it arrives in your mailbox in the second week of December?

Come for the investment. Stay for the show. Never a dull moment.

But seriously, Happy Thanksgiving! We have much to be thankful for. (Including my poor grammar).

They have to include it, right?