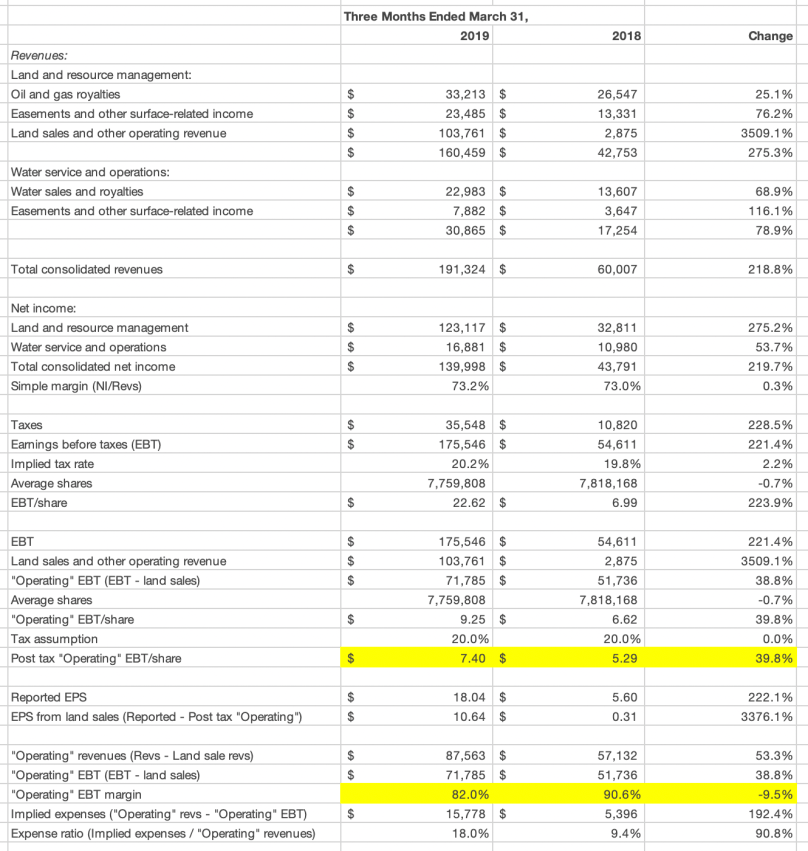

The rows below should be pretty self explanatory. Ultimately I wanted to get to earnings adjusted for asset sales. “Operating” after tax EPS is calculated to be $7.40 for Q1-19 vs $5.29 for Q1-18. Implies 39.8% growth.

Lower than normal “operating” margins stay with us. Looks like an 82.0% margin on “operating” earnings in Q1-19 vs 90.6% in Q1-18. Expenses over the same time peried (implied from data provided in the release) are estimated to be up 192%.

I’m impressed by the figures quoted immediately below. Production growth marches on!

Oil and gas royalty revenue was $33.2 million for the first quarter ended March 31, 2019, compared with $26.5 million for the first quarter ended March 31, 2018, an increase of 25.1%. Crude oil and gas production subject to the Trust’s royalty interests increased 58.5% and 119.6%, respectively, in the first quarter ended March 31, 2019 compared to the first quarter ended March 31, 2018. While crude oil and gas production increased in the first quarter ended March 31, 2019 compared to March 31, 2018, the prices received for crude oil and gas production decreased 16.7% and 46.7%, respectively, over the same time period.

The last column in the exhibit above should read 1Q19.

I rest my case. Land sales to pump up the General’s election is a dilution of trust assets forever. Do they think that we are witless? I mentioned in a previous comment the lack of information on how many DUCs and producing wells were on the land that they sold, and did they retain royalty interests?

LikeLiked by 1 person

The land sales happened before the General came on the scene, this election had nothing to do with it. The Trust is a “self-liquidating trust” and selling land is what it is set-up to do. The purpose was to selloff all the remaining properties, so land sales are normal and expected. And then the Permian happened….

LikeLiked by 1 person

I agree with you, I think that they only have 30 days for a 1035 or 1231 exchange on the tax issue.

My comment was about the timing of the earnings release and the General’s video. They should not have been on the same day. Fortunately, from the stock’s drop today, most people are seeing the real operating earnings, not the one’s the would like us to by joyous about.

LikeLiked by 1 person

They sold the royalty acres .Seems unpardonable!

LikeLiked by 1 person

The biggest disappointment to me is buying in less than 1% of the stock for the year in a year that the stock went into the low 400’s. Criminal. Its almost like they don’t want to make horizons ownership position larger. It is one of the things that is unique about this stock.

LikeLiked by 1 person

Exactly, but I think that the $400’s was actually in 4th Qtr 2018, but no matter, they should have been buying.

LikeLiked by 1 person

Good job at analysis. Didn’t they have 6-months before having to realize a profit, so that they could go out and purchase properties to offset this capital gain? And I thought that a large portion of that $100MM was reinvested already. Where were the stock buybacks? I guess it all went to the TPWR

LikeLiked by 1 person

Any idea why the disclosed land sale in the Q1 earnings release doesn’t match with previous disclosures about the sale (previously, they disclosed the sale of 14k acres at over $7k/acre).

LikeLiked by 1 person

I don’t know. My comment about these being the proceeds of the WPX sale might be wrong. Need the Q to be certain.

LikeLiked by 1 person