The Hex

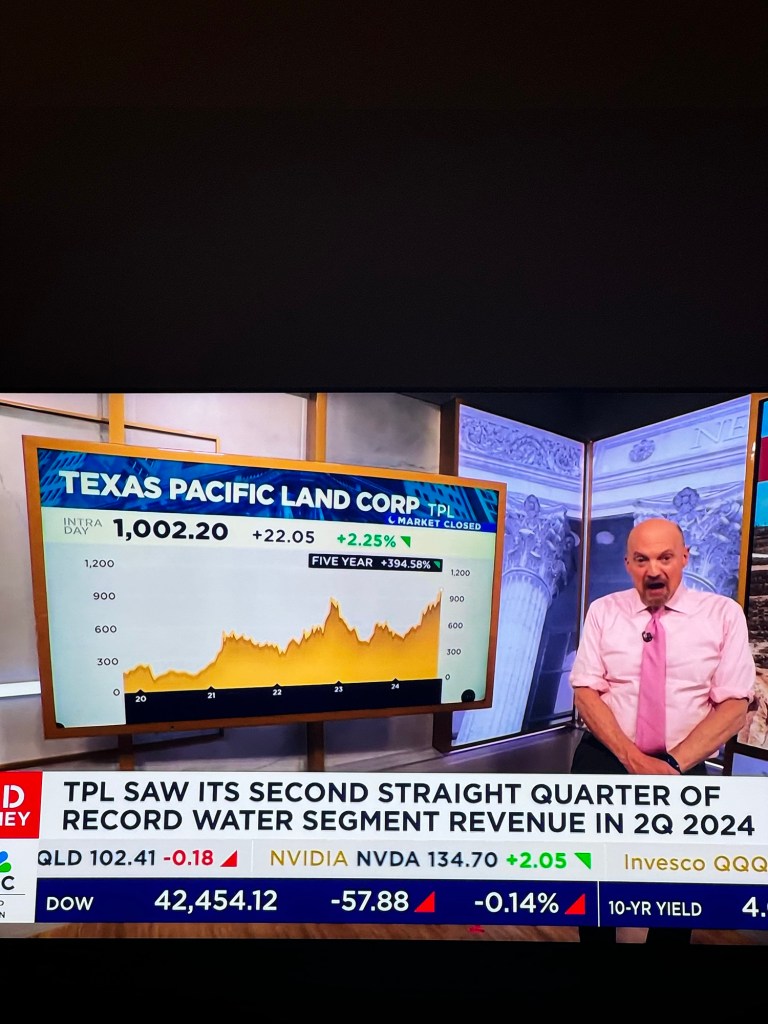

$1000/$3000 (for my pre-split folks). $22.978B mkt cap. Congrats to all the long term holders out there!

Let’s use the remaining share authorization to get back down to $333 so the climb to $1000 can start anew. Hmmmm? Hmmmmmm?

The sun never sets on the TPL empire.

Per Thefly.com, TPL options have been listed.

#6 has passed twice already. Last year it was #7. How many more times does it has to pass until the board does something about it?

#4, on the other hand, is the real deal.

https://www.sec.gov/ix?doc=/Archives/edgar/data/1811074/000110465924093445/tm2422814d1_8k.htm

Pro-rata purchase of mineral interests with a Brigham minerals fund. Seems like a pretty effective way to get deals done. Aligned incentives.

They flew commercial, right?

https://ir.stockpr.com/tpltrust/sec-filings-email/content/0001811074-24-000049/tpl-20240630.htm

Solid and could have been more so with higher nat gas prices (fully out of control of company).

I didn’t read the fine print in recent announcements. How often will cash be swept out via div to get to $700MM? Should the regular dividend be higher with FCF healthily in excess of $100MM?

Of course, I remain thankful for another quarter of no dilution.

https://www.sec.gov/rules-regulations/shareholder-proposals/shareholder-proposals-incoming

https://www.sec.gov/files/corpfin/no-action/14a-8/specialtpl71224-14a8.pdf

https://www.sec.gov/files/corpfin/no-action/14a-8/belltpl71224-14a8.pdf

It’s that time of year again. Company is petitioning the SEC to take “no action” on two proposals this year.

The Goldstein proposal affirms my belief that there remains a large contingent of shareholders (self included) that remain steadfastly opposed to equity issuance.

New video on company main page. Very well done!

Below is a direct link in case it moves locations.

DRIPs crush the offer side of the market.

Uncle Sam thanks you for the tax receipts.

If only there was a way capital could be returned more efficiently.

Here’s the competition

LandBridge filed an S-1 on May 31st announcing its IPO. The filing has had a couple updates with the latest having taken place on Monday 6/17).

If you’re completely new to the story, this Reuters article provides a good start.

I’d recommend giving the S-1 a good skim at the very least if you are a TPL owner. Yes, they are trying to sell an IPO some consideration is needed BUT it does help illustrate the longevity and optionality inherent in West Texas surface acreage.

Equity IPO analysis isn’t my specialty but it looks like the sponsor is selling 20% of the company. 20% @ $320MM implies a market cap of $1.6B. The docs say proforma net income of $50MM which implies a P/E of 32x.

I’d love your thought on this. I’m on a plane and working though my phone. Not ideal. Missing a bunch, I’m sure.

I’ll leave you with this to ponder…

For the year ended December 31, 2022, we generated $33.5 million of non-oil and gas royalty revenue on our initial approximately 72,000 owned surface acres, or $465 in revenue per owned surface acre. As a result of our active management strategy, we have increased non-oil and gas royalty revenue on such 72,000 owned surface acres by 56% to $52.1 million for the year ended December 31, 2023, or $724 in revenue per owned surface acre. We measure our revenue divided by our total acreage as a performance metric, which we refer to as “surface use economic efficiency.” We believe that the Acquired Lands present an attractive opportunity to apply our active land management strategy in a similar fashion and generate attractive returns for our investors.