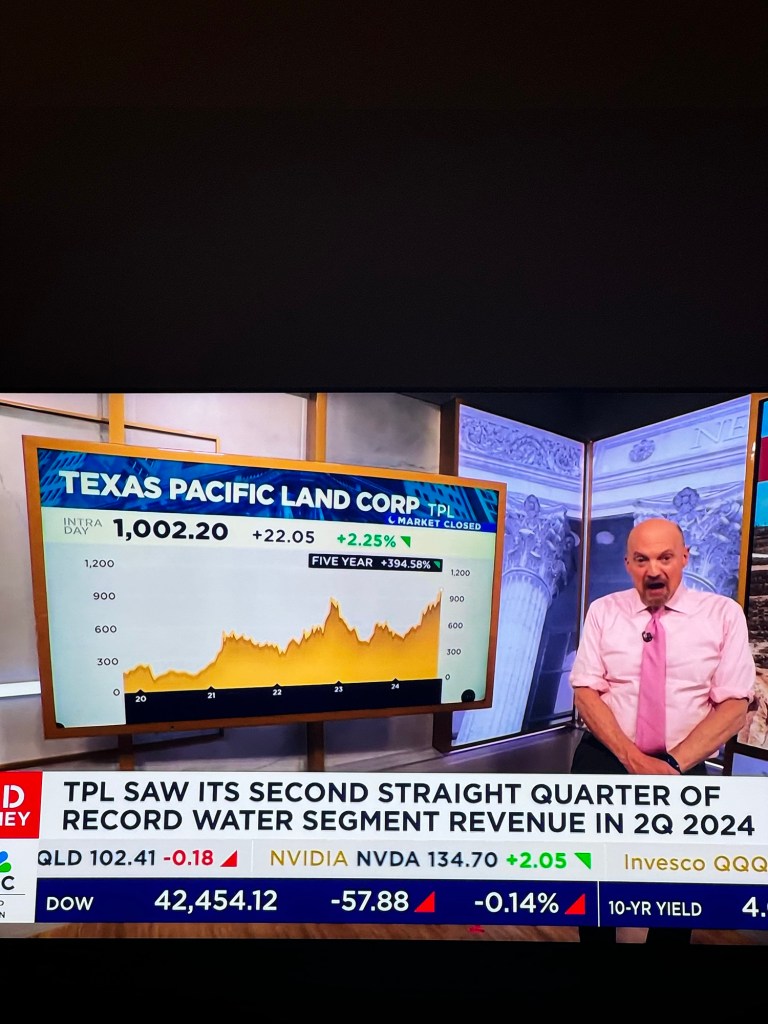

It’s no secret that I think TPL’s capital allocation policy is a joke. The cost of equity capital, measured over any timeframe, is well in excess of the implied return of an asset sold in any kind of market that is near competitive. Each day that a buyback has not been made is a day that has cost investors money. With the stock at ATHs, it’s easy to say that the stock is rich, but then again, it makes ATHs all the time. The Board eats up all the old tropes about valuation and attractive assets because everyone is incentivized to keep on making inefficient decisions. You’ve heard this all from me before…

Anyhow, our old pal 310 has put pen to paper to quantify just how much the “dry powder” strategy has hurt. It’s not pretty.